India’s Budget Points to Slower Fiscal Deficit Reduction

Feb 08, 2022, 09:46 IST

Fitch Ratings-Hong Kong: The higher deficits and continued lack of clarity on medium-term consolidation plans in India’s latest budget add risks to Fitch Ratings’ projection of a downward trajectory in government debt/GDP. The degree to which planned higher capex supports GDP growth and offsets these risks is an important consideration for the sovereign rating. Risks around the sustainability of the downward debt trajectory were a key factor behind our decision to maintain a Negative Outlook when we affirmed India’s ‘BBB-’ rating in November 2021.

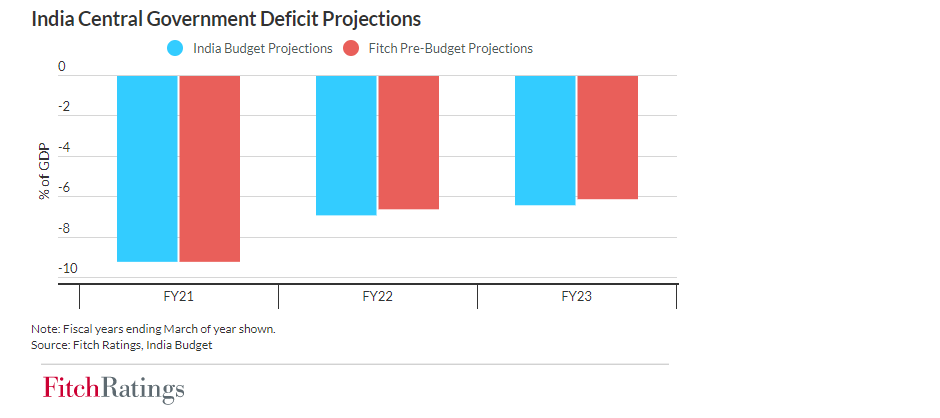

The Union budget presented by the government on 1 February 2022 continued to emphasise support for growth over fiscal consolidation. Deficit targets were slightly higher than we had anticipated when we affirmed the rating; the budget flags a revised deficit of 6.9% of GDP for the fiscal year ending March 2022 (FY22), against our 6.6% forecast. The planned 6.4% of GDP FY23 deficit is also higher than our 6.1% forecast. The borrowing allowance for states, which was maintained at 4.0% of gross state domestic product in FY23, keeping it above the pre-pandemic level of 3.0%, poses further risk to our fiscal forecasts.

The higher deficit in FY22 reflects greater capex, which is partly to clear Air India’s liabilities, as well as increased spending in response to Covid-19 virus outbreaks and shortfalls on divestments. Revenue receipts, excluding divestments, were 16% above the targets in last year’s budget.

The government plans to raise FY23 capex by 24% above the revised FY22 estimates to around 2.9% of GDP. The budget sees revenue receipts, excluding divestments, increasing by about 9.6% from revised FY22 estimates and the divestment target is set at INR650 billion (0.3% of GDP), against a revised estimate of INR780 billion in FY22.

We believe the budget offers a degree of confidence in the near-term fiscal outlook. The nominal GDP growth target for FY23 of 11.1% looks credible and revenue targets, including those for divestments, are realistic. The government also appears to be following through on its efforts to improve budget transparency by keeping previously off-budget spending on budget, limiting downside surprises.

However, there is less clarity around the medium-term outlook. The broad target of reducing the deficit to 4.5% of GDP by FY26 remains, but the budget offered few details on how this will be achieved. The higher FY23 deficit also implies significant fiscal tightening between FY24 and FY26 to meet the target. Fiscal consolidation tended to fall short of government goals prior to the pandemic, suggesting risks to the medium-term target and debt trajectory.

The planned acceleration in infrastructure capex will provide a fillip to near- and medium-term growth, if fully implemented. This could offset downside risks to our real GDP growth forecast, which stands at 10.3% in FY23 and about 7% on average through to FY27. The downside risks include disruption to economic activity associated with the Covid-19 pandemic, recent reform slippage and weakness in household income growth, which may constrain the capacity of private consumption to support growth. The budget provided no significant new transfers to households or major structural reform initiatives.

India’s public debt/GDP ratio, at about 87% in FY21, is well above the median of around 60% for ‘BBB’ rated sovereigns. We revised the Outlook on India’s rating to Negative, from Stable, in June 2020, partly owing to our assumptions about the impact of the pandemic on public finance metrics. The government has little fiscal headroom at its current rating level to respond to possible shocks to growth.

Advertisement

Top Stories

Rourkela, March 20 (IANS) Researchers from the National Institute of Technology (NIT) Rourkela have developed an Internet of Things-enabled smart device to monitor the quality of ingredients in processed food.

Andhra Pradesh

Telangana

Politics

Entertainment

Crime

Video