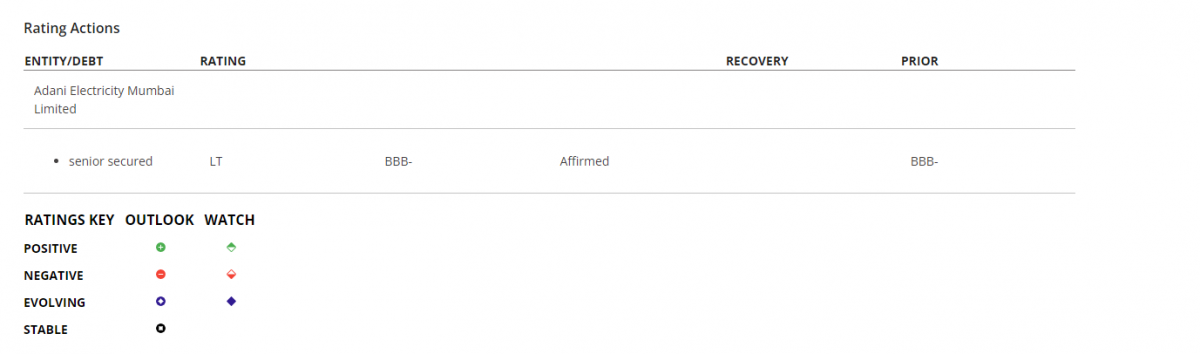

Fitch Affirms Adani Electricity Mumbai's USD Notes at 'BBB-'

Feb 08, 2022, 10:38 IST

Fitch Ratings - Singapore: Fitch Ratings has affirmed the 'BBB-' rating on India-based Adani Electricity Mumbai Limited's (AEML) US dollar senior secured notes due in 2030. Fitch has also affirmed AEML's USD2 billion global medium-term note (GMTN) programme and notes issued under the programme at 'BBB-'.

The 2030 notes and notes issued under the GMTN programme represent joint and several obligations of AEML and Power Distribution Service Limited (PDSL) - together referred to as the obligor group. AEML is 74.9% owned by Adani Transmission Limited (ATL, BBB-/Negative), while PDSL is a subsidiary of ATL that collects AEML's corporate expense allocations and keeps the receipts within the obligor group for the benefit of the US dollar noteholders.

The credit assessment benefits from the regulated nature of AEML's assets across generation, transmission and distribution wires, and supply businesses, which provide cash flow certainty. AEML has low counterparty risk, with direct exposure to retail customers in India's commercial hub, Mumbai. Construction risk is also low as the majority of planned investments are granular capex approved by the regulator.

However, the obligor group's credit assessment of 'bbb-' is weighed down by low, albeit improving, interest coverage and the group's concentration on a single regulator and city. Fitch expects interest coverage, measured by EBITDA/net interest, to stay below 2.5x.

KEY RATING DRIVERS

Demand Recovers; EBITDA Resilient: Electricity offtake by AEML's commercial and industrial customers increased by 15.6% yoy in the first half of the financial year ending March 2022 (FY22), after falling by a similar amount in FY21 due to measures to curb the spread of Covid-19. The AEML obligor group's EBITDA, adjusted for accrued income, rose by 6% in the 12 months to September 2021 after rising by 4% in FY21. The EBITDA increases reflect the stable cost-plus regulatory framework, despite lower off-take by customers.

We believe the group's regulatory assets of INR6.2 billion at end-September 2021 will allow for accrued income to be recovered through a tariff adjustment in the regulator's mid-term review. AEML's cash collection also remained strong, at 103.5% in 1HFY22, and receivable days recovered to 51 in 1HFY22 (FY21: 59). AEML's capex increased in 1HFY22 to INR7.8 billion (1HFY21: INR4.2 billion), putting it on track to exceed the INR11.9 billion in FY21 (FY20: INR12.9 billion).

Adequate Financial Metrics; Higher Capex: Fitch expects the obligor group to maintain an adequate financial profile, with EBITDA/net interest remaining above 2.3x, and leverage, defined as net debt/EBITDA, staying below 5.0x over the medium term, even after factoring in additional capex. Fitch expects AEML's capex to average around INR20 billion a year from FY22 to FY24. Fitch expects the obligor group's financial metrics to be supported by an increase in EBITDA to INR24.5 billion by FY24 (FY21: INR16.6 billion) as planned investments are commercialised.

Stable Regulatory Framework: AEML benefits from a favourable regulatory environment. Revenue from all its business segments - generation, transmission and distribution wires, and supply - is based on a cost-plus tariff, which provides long-term cash flow certainty and stability. Maharashtra's state electricity regulatory commission has a long record of delivering predictable outcomes, including tariffs. We believe any delay in recovering accrued income during the pandemic will be recouped with interest costs on any incremental working-capital borrowings, in line with regulations.

Cash Flow Visibility: AEML, aside from its supply business, does not face sales volume risk and its return on capital is ensured by regulations as long as it hits availability benchmarks. The company's strong operating performance in excess of regulatory benchmarks also helps long-term cash flow visibility. AEML's distribution and transmission licences are valid till 2036 and the company says its Dahanu power project has a residual life of about 15 years.

Low Counterparty Risk: AEML supplies electricity to 2.5 million households directly, while another 0.6 million use its network through the open-access framework with reasonable collection rates. Residential customers contribute around 45% to revenue, with the balance from commercial and industrial customers. The risk of customers switching to other suppliers is low. AEML also incurs less incremental capex to connect customers than its competitors due to its network spread and economies of scale.

Structural Enhancements: The obligor group's credit profile is supported by structural enhancements, which are achieved through various restrictions, such as a defined cash waterfall and limits on the incurrence of additional debt. Cash distributions to shareholders are allowed subject to compliance with covenants based on the debt service coverage ratio (DSCR). Distributions fall progressively with drops in DSCR levels, with no distributions if the DSCR falls below 1.35x (1HFY22: 5.80x).

Lack of Regulatory, Geographical Diversification: AEML's business is integrated across generation, transmission and distribution wires, and supply segments, but exposure is limited to one regulator - Maharashtra's electricity regulatory commission - and a single city. We believe the limited regulatory exposure carries high political risk, which weighs on the obligor group's credit assessment of 'bbb-', along with the modest interest coverage.

DERIVATION SUMMARY

We assess Power Grid Corporation of India Ltd's (POWERGRID, BBB-/Negative) Standalone Credit Profile (SCP) at 'bbb+', two notches above obligor group's credit assessment on account of POWERGRID's stronger financial profile and exposure to the central electricity regulator, which we believe has lower political risk than a state electricity regulator. AEML's counterparty risk is lower, with direct exposure to retail customers in India's commercial hub of Mumbai.

POWERGRID has indirect exposure to state-owned distribution companies, which have weak credit profiles, but the counterparty risk is mitigated by a pool-based payment mechanism and tripartite agreements, the indispensable nature of transmission assets and a lower transmission tariff contribution in the total electricity tariff on average.

London Power Networks plc's (BBB+/Stable) ratings reflect its stable, fully regulated earnings under a better operating environment than the AEML obligor group's, solid performance against regulatory targets, and strong financial projections. The better business and financial profiles justify London Power Networks' two-notch higher rating than the credit assessment of the AEML obligor group.

We assess AEML's credit profile as similar to that of NTPC Limited (BBB-/Negative, SCP: bbb-) with both having similar financial metrics. NTPC's counterparty risk is higher, as the group has power-purchase agreements with Indian state-owned distribution companies, which have weak credit profiles. However, this is mitigated by its dominant market position as it supplies more than 20% of India's electricity, reasonable average electricity tariffs and tripartite agreements. NTPC's exposure to the central electricity regulator has lower political risk than AEML's exposure to a single state regulator. The Negative Outlook on NTPC reflects the Negative Outlook on the Indian sovereign (BBB-/Negative), its parent.

KEY ASSUMPTIONS

Fitch's Key Assumptions Within Our Rating Case for the Issuer

- Revenue based on relevant costs, regulated return on equity and incentive income linked to asset availability

- Actual operation and maintenance costs at 5% more than that allowed in the tariff

- Additions to regulated asset base of about INR12 billion in FY22 and INR18 billion in FY23

- Capex to average around INR20 billion per year from FY22 to FY24

RATING SENSITIVITIES

Factors that could, individually or collectively, lead to positive rating action/upgrade:

Any positive rating action on the notes is subject to an upgrade of India's Country Ceiling of 'BBB-' and an improvement in the obligor group's financial profile as detailed below, provided there is no material deterioration in its business risk profile:

- EBITDA/net interest coverage sustained above 2.5x (FY21: 2.4x) and net leverage, measured by net debt/EBITDA, sustained below 5.0x (FY21: 4.8x)

- Net debt/fixed assets maintained below 68% (FY21: 59%)

Factors that could, individually or collectively, lead to negative rating action/downgrade:

- Downward revision of India's Country Ceiling

- EBITDA/net interest coverage below 2.0x for a sustained period

- Net leverage above 6.0x for a sustained period

- Net debt/fixed assets above 73% for a sustained period

BEST/WORST CASE RATING SCENARIO

International scale credit ratings of Non-Financial Corporate issuers have a best-case rating upgrade scenario (defined as the 99th percentile of rating transitions, measured in a positive direction) of three notches over a three-year rating horizon; and a worst-case rating downgrade scenario (defined as the 99th percentile of rating transitions, measured in a negative direction) of four notches over three years. The complete span of best- and worst-case scenario credit ratings for all rating categories ranges from 'AAA' to 'D'. Best- and worst-case scenario credit ratings are based on historical performance. For more information about the methodology used to determine sector-specific best- and worst-case scenario credit ratings, visit https://www.

LIQUIDITY AND DEBT STRUCTURE

Strong Liquidity: AEML's liquidity is supported by the bullet maturity of its US dollar notes, which account for the majority of its debt. The company had readily available cash of INR18.7 billion at end-1HFY22 against short-term debt maturities of INR8.3 billion. We believe AEML has ready access to working-capital facilities due to its regulated asset base should it face a delay in cash collections. We expect AEML to start streaming cash to ATL from FY23 after compliance with the waterfall structure defined in the indenture of the bonds.

ISSUER PROFILE

AEML, whose other shareholder is Qatar's sovereign wealth fund, operates the integrated generation, transmission and distribution utilities powering 85% of Mumbai. AEML's distribution network spans over 470 square kilometres, catering to the electricity needs of over three million customers, reaching two out of three households in Mumbai.

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

ESG CONSIDERATIONS

Unless otherwise disclosed in this section, the highest level of ESG credit relevance is a score of '3'. This means ESG issues are credit-neutral or have only a minimal credit impact on the entity, either due to their nature or the way in which they are being managed by the entity. For more information on Fitch's ESG Relevance Scores, visit www.fitchratings.com/esg

Advertisement

Top Stories

Ugadi or Yugadi is an important Hindu festival that heralds the arrival of a new year in the Hindu lunisolar calendar. This year, Ugadi will fall on March 30, 2025, and will be celebrated with much fervor in the southern states of Andhra Pradesh, Telangana, and Karnataka.

Andhra Pradesh

Telangana

Politics

Entertainment

Crime

Video