Stronger Dollar Remains a Risk for Emerging-Market Sovereigns

Feb 23, 2022, 12:05 IST

Fitch Ratings-London/Hong Kong: Exchange rates against the US dollar have held up for most emerging markets (EMs) in recent months, but there remains a risk that more could face significant depreciation pressure in 2022, particularly if the pace of monetary tightening in the US accelerates, says Fitch Ratings. Under such a scenario, EM sovereigns could face difficult monetary policy choices and higher repayment burdens for US dollar-denominated debt.

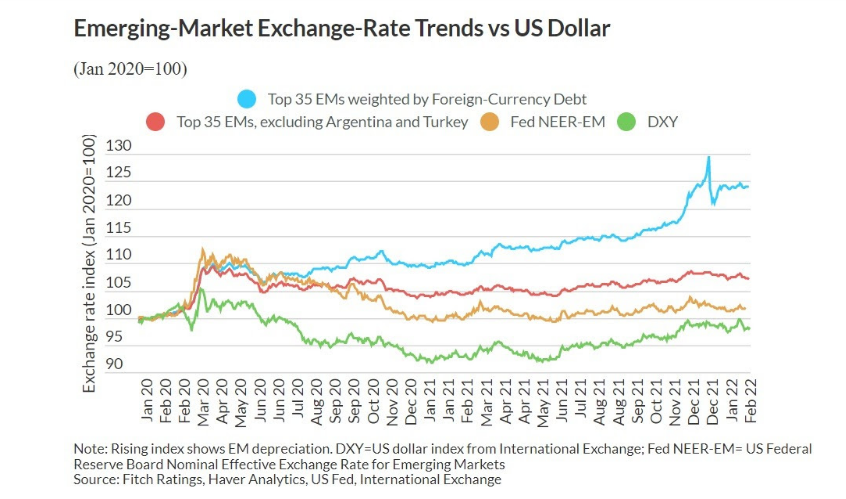

Fitch’s EM exchange rate index, which weights EMs by the value of their outstanding foreign-currency government debt, has shown a marked depreciation against the US dollar in recent months. However, this largely reflects exchange-rate movements in Turkey and Argentina, two particularly vulnerable EMs with very large volumes of outstanding foreign-currency debt.

Excluding these two countries, the index has been more stable against the US dollar, despite a marked shift in market sentiment around the expected pace of US monetary tightening. Fitch, for example, now expects US policy rates to rise by 100bp in 2022, and another 100bp in 2023, compared with our December 2021 forecasts of 25bp and 50bp, respectively.

There are reasons for the stability of most EM exchange rates. A number of EMs, such as Brazil, Chile, Poland and Russia, have raised policy rates ahead of the US tightening cycle, reducing the potential for capital outflows. In past cycles, EM rate increases often lagged behind those in the US. Inflation in the US is also higher than it has been in decades, making real interest rates there less attractive.

Nonetheless, we believe that there is still a risk that EM exchange rates could come under greater pressure this year as US monetary tightening progress. An increase in global risk aversion could also increase capital flows into US assets.

Depreciation of EM currencies against the US dollar would raise the burden associated with a higher share of foreign-currency-denominated debt obligations. Fitch estimates that EM median foreign-currency government debt increased to 31% of GDP by end-2021, from 18% in 2013, the year of the so-called "taper tantrum". This is consistent with an increase in EM median government debt to 60% of GDP from 34% over the same period combined with an increase in the median foreign-currency share of debt to 59% from 52%.

Financing current account deficits (CADs) could also grow more challenging, even as recoveries from the Covid-19 pandemic shock stoke imports in many EMs this year. Fitch believes that external vulnerabilities are concentrated among smaller EMs, and particularly weaker frontier sovereigns.

Policymakers in EMs may feel pressure to raise rates to attract capital inflows or to prevent depreciation that might threaten inflation targets, or financial stability where balance sheets are exposed to exchange-rate risk. This could weigh on growth outlooks, at least in the near term, and so complicate the task of fiscal consolidation for EMs in the wake of the pandemic. For countries with short average local-currency debt maturities and high debt levels, it could also push up interest/revenue ratios, which are already high for a number of EM sovereigns.

Offsetting factors may support growth for some EMs. Inasmuch as a stronger US dollar would reflect higher US rates designed to cool demand-led inflation in the US, it may be associated with robust near-term external sector prospects. However, Fitch forecasts US growth to slow to 1.9% in 2023 from 3.7% in 2022. Commodity-exporting EMs may also benefit from relatively high prices, notably for energy, which have contributed to the tightening of US monetary policy.

More from section

Advertisement